Over recent years, news headlines have been bombarded with stories of disillusionment that recent grads face as they head into their professional career, in terms of salary expectations and how quickly they must start paying back student loan debt.

This becomes trickier as entrepreneurial-minded grads decide to work at a startup before they start one. “Early in your career, what’s most important is to learn,” says Dave Carvajal, who built HotJobs to 650 employees, $125M revs, a IPO then sold to Yahoo! for $436M.

“If your goal is entrepreneurship, the best way to reach it is to serve with the best founders and entrepreneurs you can find. Before you can be an effective leader, you must study how leadership works, by being effectively led.”

But this comes at a cost—one that many recent grads can’t stomach.

Recent grads unrealistic about startup job market

As a founder, I hear it all the time when we are connecting job seekers with positions at high-growth startups abroad. It’s usually one of two responses: “I can’t take this opportunity because the salary won’t be enough to pay my student loans” or the quintessential “I want to make bank!” Both are inherently flawed—especially if new hires want to cut their teeth in the startup world.

Let’s start with the first assertion: “I can’t take this opportunity because I won’t be able to pay down my student loans.”

We hear this reply so much that we became curious to see how long it takes the average person to pay their student loan debt. Turns out, most people don’t make a dent in their loans throughout the first five years of their career. In reality, most don’t make a dent in their debt for the first 10 years! It takes the average person 20 years to pay off their student loan debt, according to U.S. News & World Report.

Now let’s think about this; many recent graduates are turning down great opportunities, both domestically and internationally, because of the weight of student loan debt.

Rather than objectively looking at an opportunity and saying “this is an opportunity I am passionate about and it will provide me with a great skill set and career trajectory,” they are adamant in thinking, “I’ll take a job I am less thrilled about because it will pay more money and allow me to pay my student loans off faster.” But this logic is inherently flawed.

Recent grads are taking jobs they don’t like under the illusion they will earn more money and pay off loans faster, but in reality they don’t make the dent in their loans they were hoping to make. This leads to frustration, burnout, and a career they didn’t ask for.

Now let’s look at the second assertion many fast-growth startups will hear from recent grads: “I want to make bank!”

News flash — if you haven’t graduated from an Ivy league school and/or you aren’t a software programmer or investment banker, you probably won’t be making the money you’ve dreamed of coming in at entry-level.

Recent grads often have a perception that they will be able to a) make money and b) save money. They believe they will graduate and instantly be handed a lucrative and fulfilling job with great compensation and that they’ll save a ton of money. The harsh reality is: this rarely happens.

Moreover, what many people fail to consider when they have this mentality is the cost of living in startup laden cities. For example, those who make upwards of 80k a year, 3 to 4 years out of school, are still saving next to nothing on a monthly basis.

Consider what this looks like in metro areas. “Single people residing in the New York City metro area, for example, might want to allocate $3,627 for monthly expenses, which amounts to over $40,000 a year (Business Insider).” Although you are making a great salary, the cost of living can be so high that you don’t actually end up saving any money.

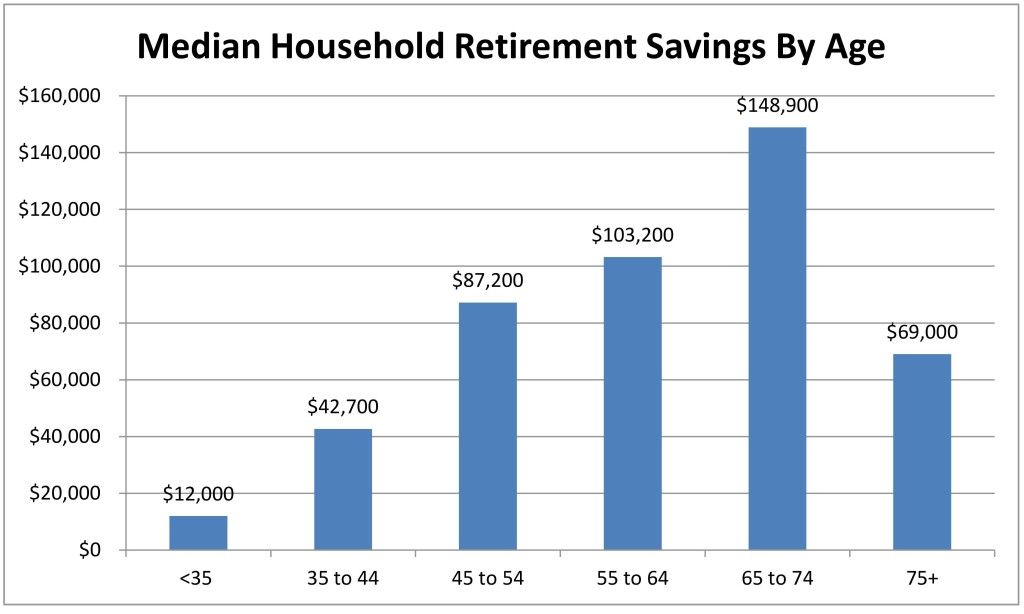

To prove this assumption, we did some digging to see what people actually save during their twenties. Turns out, most people save next to nothing. Instead, a bulk of their savings and financial stability starts in their thirties. Not what they told you in school? Yeah, us too.

So, let’s think about this . . . many recent grads are overloaded with student debt and choose jobs they mistakenly believe will allow them to pay off student loans, while others have their sight set on jobs with financial security (that doesn’t really exist).

Seems pretty flawed when you think about it this way, right?

Replace flawed logic with profitable perspective

In reality, this paints a picture of is a much larger problem. During your twenties, you probably won’t save much money or actually pay off a bulk of your student loan debt. It’s a hard truth, but if you understand this, you will break the cycle of letting compensation be the primary factor for evaluating a job opportunity.

Instead, you should choose a position that allows for you to learn, grow, and take on new responsibility. Take a job that will:

-

provide you with a skill set you can take anywhere.

-

enable you to learn something you are passionate about (that may come with less pay).

-

be fulfilling, something you can look back on and say, “Wow! I absolutely loved doing that!”

Next, realize that the bulk of your savings will come in your thirties, when you have developed a marketable skill set you do well and can get rewarded for how

well you do it. Realize that financial stability comes with age, and remaining patient and intrinsically motivated is a much larger predictor of your

success than the money you earn as a recent grad.

Ultimately, your twenties are for learning, while your thirties are for earning.

This article has been edited and condensed.

Matt Williams is the co-founder and Head of Marketing at BrainGain. BrainGain connects job seekers with career relevant positions at high-growth startups in emerging economies. Connect with @teambraingain on Twitter.

© YFS Magazine. All Rights Reserved. Copying prohibited. All material is protected by U.S. and international copyright laws. Unauthorized reproduction or distribution of this material is prohibited. Sharing of this material under Attribution-NonCommercial-NoDerivatives 4.0 International terms, listed here, is permitted.